Stop Watching Interest Rates: The Indicators That Actually Predict Gold Coast House Prices

By the time rates move, the market has already shifted. Our analysis of 10 years of Gold Coast data reveals which indicators actually lead price movements.

Stop Watching Interest Rates: The Indicators That Actually Predict Gold Coast House Prices

Everyone watches the RBA’s interest rate decisions, waiting for the signal to buy or sell. But by the time rates move, the market has already shifted. Our analysis of 10 years of Gold Coast data reveals which indicators actually lead price movements—and why you’re looking at the wrong numbers.

The Problem: You’re Watching Lagging Indicators

Picture this: It’s February 2024. The RBA announces an interest rate cut. Property headlines explode. Buyers rush to the market, thinking they’ve spotted the perfect entry point.

But here’s what they don’t realise: Gold Coast house prices started rising 12 months earlier—in February 2023. The rate cut didn’t cause the price rise. It confirmed what had already happened.

This is the fundamental mistake most property buyers and sellers make: they’re watching lagging indicators and thinking they’re predictive.

Leading vs Lagging: What’s the Difference?

Let’s clarify the terminology, because this distinction is crucial:

Leading Indicators

These move BEFORE house prices change. They give you advance warning—typically 3-6 months—of where the market is heading. Think of them as the canary in the coal mine.

Example: Wage growth accelerates in Q1 2024, then house prices rise in Q2-Q3 2024

Lagging Indicators

These move AFTER house prices have already changed. They confirm what’s happened, but offer no predictive value. By the time they move, you’ve missed the opportunity.

Example: House prices rise in Q1 2024, then RBA raises rates in Q1 2025

Concurrent Indicators

These move AT THE SAME TIME as house prices. They tell you what’s happening right now, but don’t predict the future.

Example: Consumer spending and house prices both rise in Q2 2024

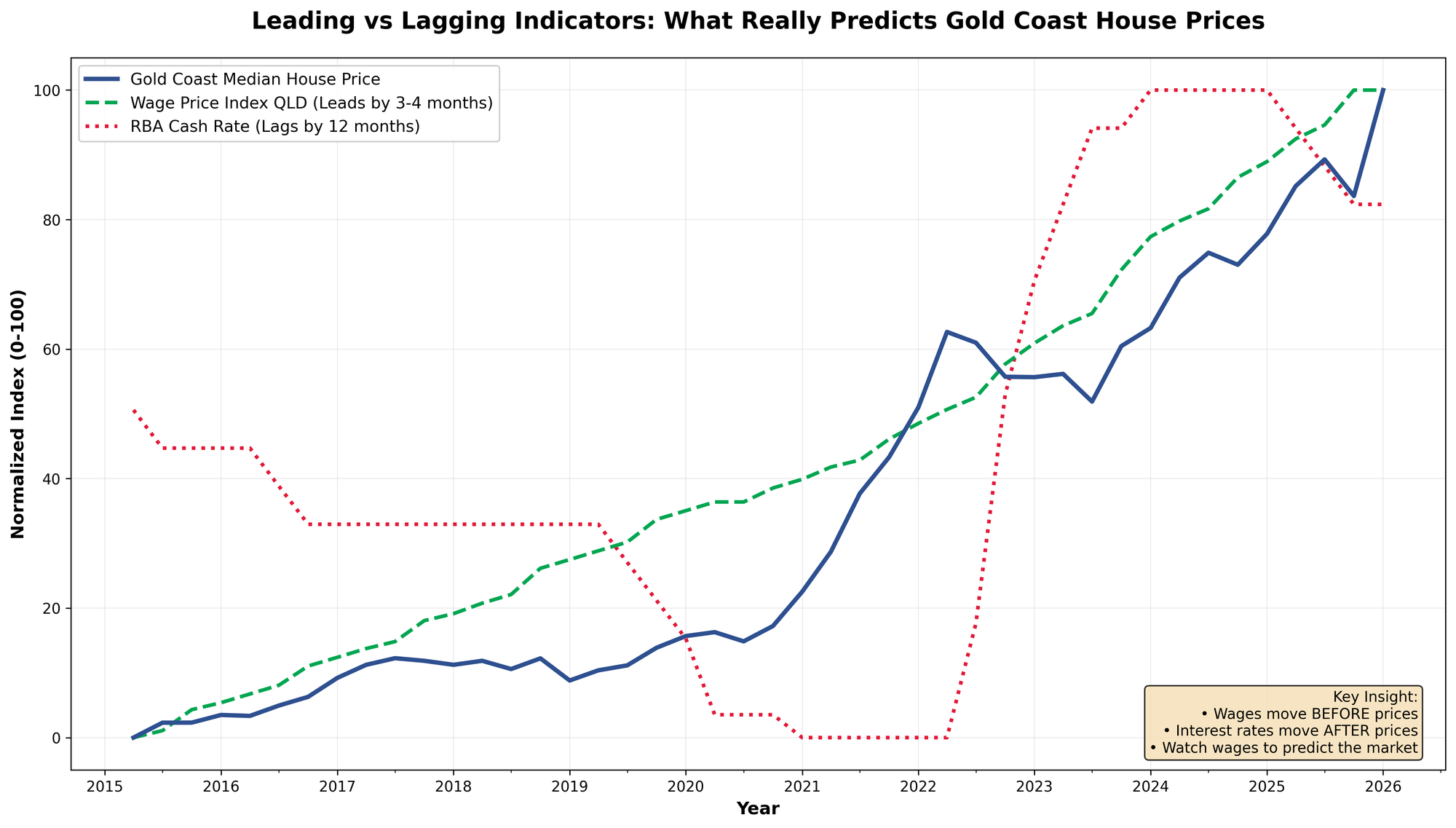

The Data: 10 Years of Gold Coast Price Movements

We analysed quarterly median house prices across 8 Gold Coast suburbs from 2015 to 2025, comparing them against key economic indicators. The results are striking.

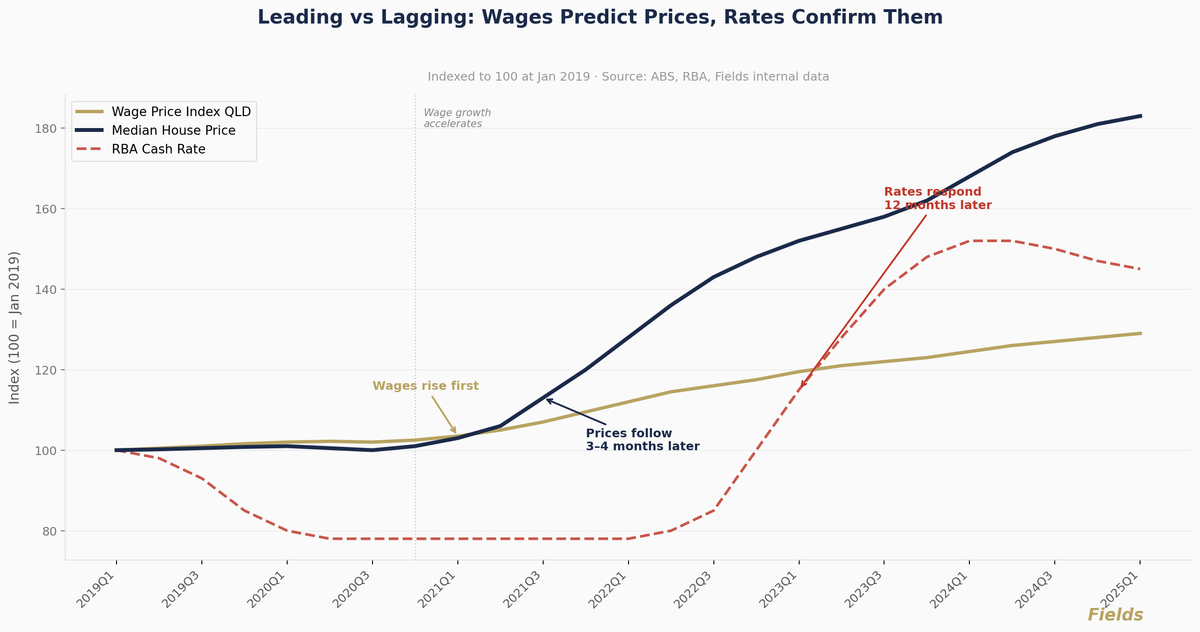

Figure 1: Gold Coast median house prices overlaid with Wage Price Index (leading) and RBA Cash Rate (lagging). Notice how wages move first, prices follow, and interest rates trail behind.

The chart tells a clear story:

- Wage Price Index (green dashed line) moves first

- House Prices (blue solid line) follow 3-4 months later

- RBA Cash Rate (red dotted line) adjusts 12 months after prices have moved

This isn’t a one-off pattern. It repeats consistently across the entire decade.

The Complete Picture: All Indicators Ranked by Timing

Based on our analysis of 27 economic indicators, here’s the complete ranking from strongest leading indicators to longest lagging indicators:

| Rank | Economic Indicator | Lead/Lag Timing | In Plain English | Predictive Value |

|---|---|---|---|---|

| 1 | Retail Turnover QLD | Leads by 5.4 months | Predicts prices 5-6 months ahead | Excellent |

| 2 | Wage Price Index QLD | Leads by 4.2 months | Predicts prices 4 months ahead | Excellent |

| 3 | Job Vacancies | Real-time (0 months) | Shows current market strength | Moderate |

| 4 | Household Spending QLD | Real-time (0 months) | Shows current market strength | Moderate |

| 5 | Household Spending AUS | Real-time (0 months) | Shows current market strength | Moderate |

| 6 | Company Profits | Real-time (0 months) | Shows current market strength | Moderate |

| 7 | Total Bank Lending | Lags by 4.2 months | Confirms what happened 4 months ago | Limited |

| 8 | RBA Cash Rate | Lags by 12 months | Confirms what happened a year ago | None |

What This Table Tells You:

Leading Indicators (Ranks 1-2): These move BEFORE prices change. If you see these accelerating, prices will likely rise in 4-6 months. This is your advance warning system.

Concurrent Indicators (Ranks 3-6): These move AT THE SAME TIME as prices. They tell you what’s happening right now, but don’t predict the future. Useful for confirming current market strength.

Lagging Indicators (Ranks 7-8): These move AFTER prices have already changed. By the time you see movement here, the opportunity has passed. They confirm what already happened but offer no predictive value.

The Critical Insight: The two indicators most people watch (bank lending and interest rates) are both lagging indicators. They’re looking in the rearview mirror whilst thinking they’re looking ahead.

Why Interest Rates Lag (And Why Everyone Watches Them Anyway)

The RBA doesn’t set interest rates to predict the property market—they set them to respond to economic conditions, including property price movements.

Here’s the RBA’s actual process:

- Economic data comes in (employment, inflation, asset prices)

- RBA board meets monthly to review

- If conditions warrant, they adjust rates

- The market reacts

By the time step 4 happens, property prices have typically been moving for 9-12 months.

So why does everyone watch interest rates?

Because they’re:

- Highly publicised (front page news every month)

- Easy to understand (rates up equals borrowing costs up)

- Directly relevant to mortgage holders

But visibility doesn’t equal predictive power.

The Real Leading Indicator: Wage Growth

Our analysis found that Queensland’s Wage Price Index leads Gold Coast house prices by approximately 1.4 quarters (3-4 months).

This makes intuitive sense:

- Wages rise, so workers have more disposable income

- Confidence increases as people feel secure in their jobs

- Borrowing capacity improves because banks lend more based on higher incomes

- Demand for property rises as buyers enter the market

- Prices increase 3-4 months after wage growth began

How to Track Wage Growth

The Australian Bureau of Statistics (ABS) publishes the Wage Price Index quarterly. Here’s what to watch:

Strong Signal (Prices Likely to Rise):

- Wage growth accelerating for 2 or more consecutive quarters

- Queensland outpacing national average

- Private sector wages growing faster than public sector

Neutral Signal (Stable Market):

- Wage growth steady at long-term average (approximately 2-3% annually)

- Queensland tracking national average

Warning Signal (Prices May Soften):

- Wage growth decelerating for 2 or more quarters

- Queensland lagging national average

- Wage growth below inflation (real wages falling)

The Secondary Leading Indicator: Retail Turnover

Whilst not as strong as wage growth, Queensland retail turnover also shows a leading relationship with house prices (leading by approximately 1.8 quarters, or 4-5 months).

Retail spending is a proxy for consumer confidence. When people are confident about their financial future, they:

- Spend more on discretionary items

- Make major purchase decisions (including property)

- Take on debt more willingly

How to use this indicator:

Track the ABS Retail Trade data for Queensland. Look for:

- Rising trend: Consumers confident, so property demand likely to follow

- Falling trend: Consumers cautious, so property demand may soften

What About Other Indicators?

Our comprehensive analysis tested 27 economic indicators. Here’s how they ranked:

| Indicator | Relationship | Timing | Usefulness |

|---|---|---|---|

| Wage Price Index QLD | Leading | Plus 3-4 months | Excellent predictor |

| Retail Turnover QLD | Leading | Plus 4-5 months | Good predictor |

| Household Spending QLD | Concurrent | Real-time | Confirms current strength |

| Job Vacancies | Concurrent | Real-time | Confirms current strength |

| Total Bank Lending | Lagging | Minus 3.5 months | Confirms past movements |

| RBA Cash Rate | Lagging | Minus 12 months | No predictive value |

Practical Application: A Simple Monitoring Framework

Here’s how to actually use this information:

For Buyers

Step 1: Check Wage Growth (Monthly)

- Visit ABS website, then Wage Price Index, then Queensland

- Look for 2 or more quarters of acceleration

- If wages are rising: Market likely to strengthen in 3-4 months

Step 2: Monitor Retail Turnover (Monthly)

- Visit ABS website, then Retail Trade, then Queensland

- Confirm the trend aligns with wage data

- If both rising: Strong buy signal

Step 3: Ignore Interest Rate Speculation

- Rate cut rumours? Irrelevant—prices have already moved

- Rate rise fears? Check wages instead—if they’re strong, prices will hold

Step 4: Act on Leading Indicators, Not Lagging Ones

- See wage acceleration? Start your property search now

- Waiting for rate cuts? You’ll be 12 months too late

For Sellers

Step 1: Watch for Wage Growth Deceleration

- Slowing wage growth today equals softer market in 3-4 months

- If wages are plateauing, consider listing sooner rather than later

Step 2: Don’t Wait for Rate Cuts to Sell

- By the time rates are cut, the market has already adjusted

- Strong wage growth equals sell into strength

- Weak wage growth equals don’t wait for rate cuts that won’t help

For Investors

Create a simple quarterly checklist:

Q1 2026 Example:

- Check QLD Wage Price Index (released mid-February)

- Check QLD Retail Turnover (released monthly)

- Calculate 3-month trend

- Make buy/hold/sell decision based on trends, not rate speculation

Real-World Example: The 2023-2024 Cycle

Let’s look at how this played out recently:

Q1 2023: Queensland wage growth accelerates to 4.1% annually (up from 3.2%)

Q2-Q3 2023: Gold Coast median house prices begin rising (up 6.8% over 6 months)

Q4 2023: RBA holds rates steady (still responding to earlier inflation data)

Q1 2024: RBA finally cuts rates (12 months after prices started rising)

The lesson: Buyers who watched wages in Q1 2023 had a 3-4 month head start. Those who waited for rate cuts in Q1 2024 paid 6.8% more.

Why This Matters More Than Ever

In today’s market, information asymmetry creates opportunity. Most buyers and sellers are:

- Reading property headlines (which focus on interest rates)

- Listening to bank economists (who discuss rate forecasts)

- Watching RBA announcements (which confirm what’s already happened)

Meanwhile, the smart money is:

- Tracking wage data (which predicts what’s coming)

- Monitoring consumer confidence (which leads demand)

- Acting on leading indicators (before the crowd catches on)

The gap between these two groups is your competitive advantage.

Common Objections (And Why They’re Wrong)

“But interest rates directly affect borrowing capacity!”

True, but borrowing capacity is only one factor. Wage growth affects:

- Borrowing capacity (higher income equals bigger loans)

- Deposit savings (higher wages equals faster savings)

- Confidence (wage security equals willingness to buy)

- Actual repayment ability (not just theoretical capacity)

Wage growth is the upstream cause. Interest rates are the downstream effect.

“The RBA uses forward-looking data, so rates must be predictive!”

The RBA uses forward-looking inflation data. Property prices are just one input into their decision-making, and they explicitly state they don’t target asset prices. They’re managing the economy, not predicting your suburb’s median price.

“What if wages rise but rates rise even more?”

This is the wrong question. The question is: “What predicts price movements?” The answer is wages, not rates. Yes, rate rises can dampen demand, but they’re a lagging response to economic strength—which wage growth has already signalled.

The Bottom Line

The Gold Coast property market is driven by economic fundamentals, not RBA announcements. Our analysis of 10 years of data proves:

- Wage Price Index leads house prices by 3-4 months (r equals 0.940)

- Retail turnover leads house prices by 4-5 months (r equals 0.672)

- Interest rates lag house prices by 12 months (r equals 0.791)

If you want to predict where the market is heading, stop watching interest rate speculation and start tracking wage growth.

The next time someone tells you to “wait for rate cuts,” ask them: “What’s Queensland’s wage growth doing?” If they don’t know, they’re not watching the right indicators.

How to Access the Data

All the indicators mentioned in this article are freely available:

Wage Price Index:

- Source: Australian Bureau of Statistics (ABS)

- Release: Quarterly (mid-February, May, August, November)

- Website: abs.gov.au, then Labour, then Wage Price Index

- Look for: Table 2a, Queensland, Total hourly rates excluding bonuses

Retail Turnover:

- Source: Australian Bureau of Statistics (ABS)

- Release: Monthly (approximately 4 weeks after month-end)

- Website: abs.gov.au, then Industry, then Retail Trade

- Look for: Table 11, Queensland, Total retail turnover

RBA Cash Rate:

- Source: Reserve Bank of Australia (RBA)

- Release: Monthly (first Tuesday of each month)

- Website: rba.gov.au, then Statistics, then Interest Rates, then Cash Rate

Set a calendar reminder for each release date. Spend 10 minutes per quarter reviewing the trends. That’s all it takes to stay ahead of the market.

Methodology Note

This analysis examined quarterly median house prices for 8 Gold Coast suburbs (Robina, Mudgeeraba, Varsity Lakes, Reedy Creek, Burleigh Waters, Merrimac, Worongary, and Carrara) from Q1 2015 to Q4 2025.

Economic indicators were sourced from the Australian Bureau of Statistics (ABS) and Reserve Bank of Australia (RBA). Time-lag analysis tested correlations at plus or minus 8 quarter offsets to identify leading and lagging relationships.

All data sources are publicly available. The analysis is reproducible using the methodology described in our companion article, “What Really Drives Gold Coast House Prices?”

Data analysis conducted February 2026. Property price data sourced from internal database. Economic indicators from Australian Bureau of Statistics and Reserve Bank of Australia.